Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If I had to draw a metaphor for our market, I would say that it feels a little like people are using Dorothy’s line “lions and tigers and bears, oh my!”

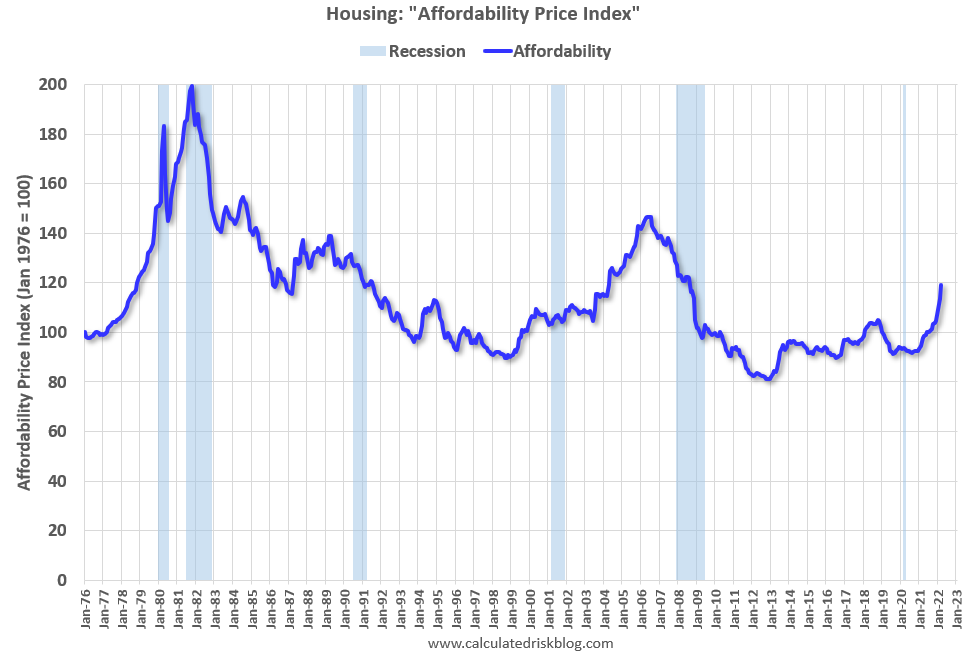

First, mortgage rates. Mortgage rates are holding high because inflation is much stickier than anticipated. Hope for rates coming down continues to be a challenge due to the unknown future with gas prices. In the last six months to a year, we’ve had a very strong correlation to rates. When rates pop up, buyers seem to get cold feet and either suspend their search and or back out of a transaction.

Second, legislation. This one has a lot to unpack. Let’s go with the low hanging fruit first: the mansion tax. Although I’m in Orange County, the mansion tax may prevent would be sellers out of LA moving to Orange County or vice versa. Asking either party to pay an additional $200,000 or more in order to complete a transaction that goes to taxes is a tough pill to swallow. The side effect of the measure results in a less mobile market overall with much heavier financial consequences for buying or selling a home.

Landlord Tenant laws is the next legislative challenge. Stories of squatters in guest homes or occupying owners’ second homes is growing. In the past, this wouldn’t have been such an issue, but with changes to landlord tenant laws, squatters are gaining tenants rights. When a squatter has tenant rights, removing the squatter becomes a long, arduous process. Many would be landlords have become deterred from owning rental property. However, one gentleman has turned this into an opportunity. To learn more about Flash Shelton, click here.

Last piece of legislation is the NAR ruling regarding buyer agent commission. This one is tough because we’re not exactly sure what this could look like. I’ve spoken with other agents and we have our two cents. These thoughts range from the first time home buyer who is properly represented is gone to why would a seller not incentivize buyers agents to bring their clients to their property. Another thought is that this opens the door for a lot of future legal problems because of Dual Agency conflict. I’ll unpack dual agency more in the future. Lastly, I think this opens the door for a record number of off market transactions. Why not try to get in touch with sellers directly for your buyers and take control of the conversation by finding the deal? This ruling will likely reduce transparency for all parties involved.

In total, I believe that all of the legislation was well intended. However, I’m not sure that the result will match the intention.